ESG matters more and more to the market and especially to the regulators

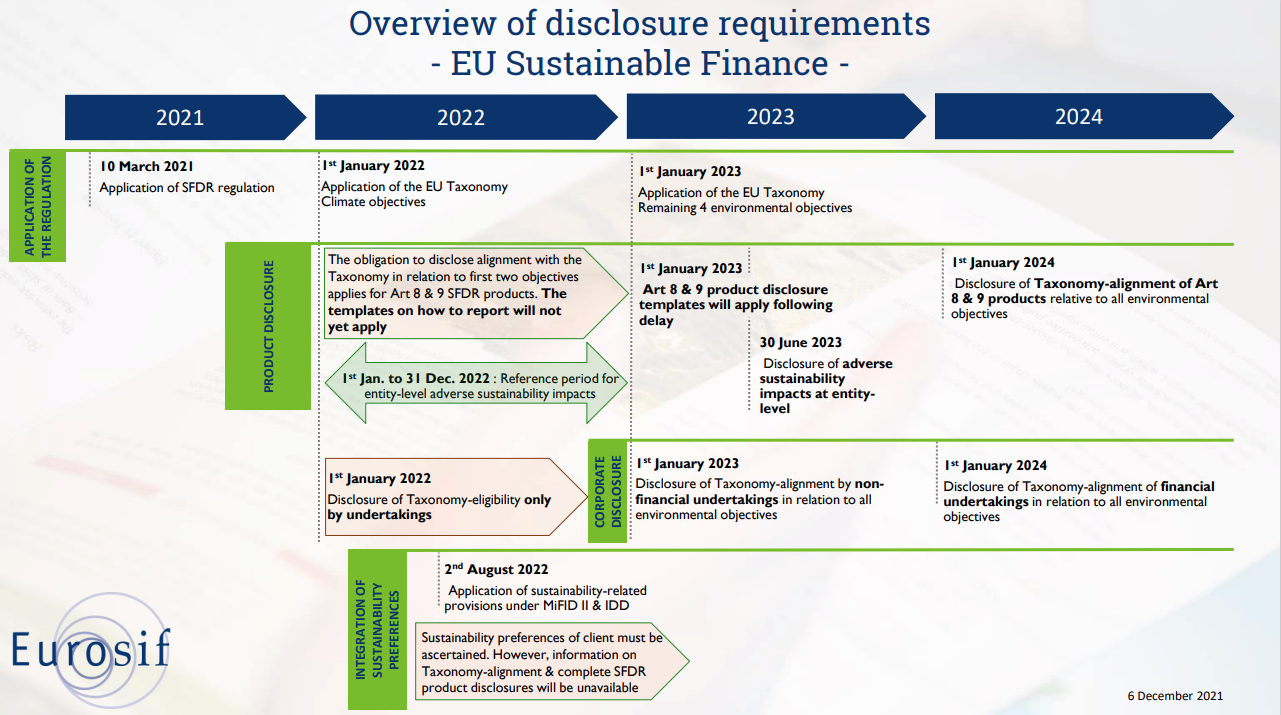

Starting January 1, 2023, SFDR Directive requires asset managers to consider and disclose in a consistent manner how ESG factors are adopted in their decision-making processes. For Articles 8 and 9 funds, this includes a Pre-contractual Disclosure (PCD), Periodic Disclosure (PD) and Website Disclosure (WD). To be classified Article 9, or ‘Dark Green Funds’, the investment strategy must have a reduction in carbon emissions as its objective. Such objectives must be tracked against an EU transition benchmark, alongside other ESG factors such as good governance procedures.

Additionally, starting June 30, 2023, asset managers will also be required to produce a Principal Adverse Impact (PAI) statement to determine the impact of their investment decisions on sustainability factors.

AIFMs in Luxembourg are under increasing pressure to disclose more ESG data to investors. Based on LGT Statistics, Only 3% of private equity funds classify themselves as dark green Article 9 strategies, i.e. those that make predominantly sustainable investments.

Within more than 300 private equity managers globally, and 57% of those has not implemented the EU’s Sustainable Finance Disclosure Regulation (SFDR).10% of the strategies surveyed in the sector define themselves as Article 8 strategies, which promote environmental and social characteristics, while 22% are classified as ‘mainstream’ Article 6 funds. One of the French PE asset managers, specializing in Mid-Cap integrates ESG related criteria in its investment decisions and portfolio management, promotes environmental and social characteristics and successfully launched the very first Art 8 PE funds.

Some Luxembourg Management Company has successfully launched UCITS Article 9-compliant real assets fund. What about Article 9-compliant real estate AIFs? According to ESMA, Funds that meet Article 9 requirements must be investing fully in investments that already qualify as sustainable. Real estate investment strategies that acquire and upgrade poor performing buildings would be in compliance with Article 9 requirements at the outset. Furthermore, the disclosure of energy-efficiency information for real estate assets might be challenging due to different energy-performance certificates (EPCs) used across Europe and in certain jurisdiction, EPCs might not be available or comparable.

In the UCITS world, it was found out that a number of Article 9 funds invest in 166 different companies that violate the UNGC or OECD principles. The violations include bribery and corruption convictions (e.g., a financial services company pleading guilty in a bribery case), anti-competitive practices (e.g., a payments company fined by FCA for collusion), and environmental impacts (e.g., a tourism-based company admitted to dumping fuel and food waste along with thousands of gallons of sewage into the ocean). Cares and solid ESG process are needed to avoid those issues and huge & challenging commitment needed reducing carbon emissions across by the portfolio company on an annual basis to support the goals of the Paris Agreement.

The war in Ukraine and the cost-of-living crisis have highlighted the ethical and social risks of complex supply chains, beyond those revealed by the pandemic, and the risks to the net-zero transition. The war has accelerated the transition to green technologies to produce energy, leading to an even faster increase in demand for the materials needed for related goods, or more energy-efficient housing especially home care or assisted living.

How have you prepared your AIFs to be in compliance with Article 8 or Article 9?

It all starts with a conversation, Let’s start ours, we are here to help and bring the change.